银行的金融数据分析外文翻译

17页

1、Banks analysis of financial dataAndreas P. Nawroth, Joachim PeinkeInstitut fu r Physik, Carl-von-Ossietzky Universita t Oldenburg, D-26111 Oldenburg, GermanyAvailable online 30 March 2007AbstractA stochastic analysis of financial data is presented. In particular we investigate how the statistics of log returns change with different time delays t. The scale-dependent behaviour of financial data can be divided into two regions. The first time range, the small-timescale region (in the range of seco

2、nds) seems to be characterised by universal features. The second time range, the medium-timescale range from several minutes upwards can be characterised by a cascade process, which is given by a stochastic Markov process in the scale . A corresponding FokkerPlanck equation can be extracted from given data and provides a non-equilibrium thermodynamical description of the complexity of financial data.Keywords: Banks; Financial markets; Stochastic processes; FokkerPlanck equation1.Introduction Fin

3、ancial statements for banks present a different analytical problem than manufacturing and service companies. As a result, analysis of a banks financial statements requires a distinct approach that recognizes a banks somewhat unique risks. Banks take deposits from savers, paying interest on some of these accounts. They pass these funds on to borrowers, receiving interest on the loans. Their profits are derived from the spread between the rate they pay for funds and the rate they receive from borr

4、owers. This ability to pool deposits from many sources that can be lent to many different borrowers creates the flow of funds inherent in the banking system. By managing this flow of funds, banks generate profits, acting as the intermediary of interest paid and interest received and taking on the risks of offering credit.2. Small-scale analysis Banking is a highly leveraged business requiring regulators to dictate minimal capital levels to help ensure the solvency of each bank and the banking sy

《银行的金融数据分析外文翻译》由会员s9****2分享,可在线阅读,更多相关《银行的金融数据分析外文翻译》请在金锄头文库上搜索。

幼儿园教育心得大班

MBR、主引导扇区主分区、扩展分区、逻辑分区活动分区、引导分区、系统分区、启动分区的区别详解

某县中心敬老院建设项目可行性策划.doc

皮克斯动画作品的成功原因.doc

会计干货之《西游记》中的财会元素(47)—物价水平看玉华.doc

建筑材料名词解释1.doc

端午习俗作文300字范文.doc

T_CIPR 0013-2023 便于紧固的铝合金模板.docx

全英文初中英语说课稿_Go_for_it__Book2_Unit_6.doc

计算机原理复习提纲(自考).doc

2022年食品安全培训心得体会

初三数学圆的知识点整理-2.docx

2022年四年级语文上册第三单元10爬山虎的脚状元预习卡无答案新人教版

完整word版-七年级地理试题及答案.doc

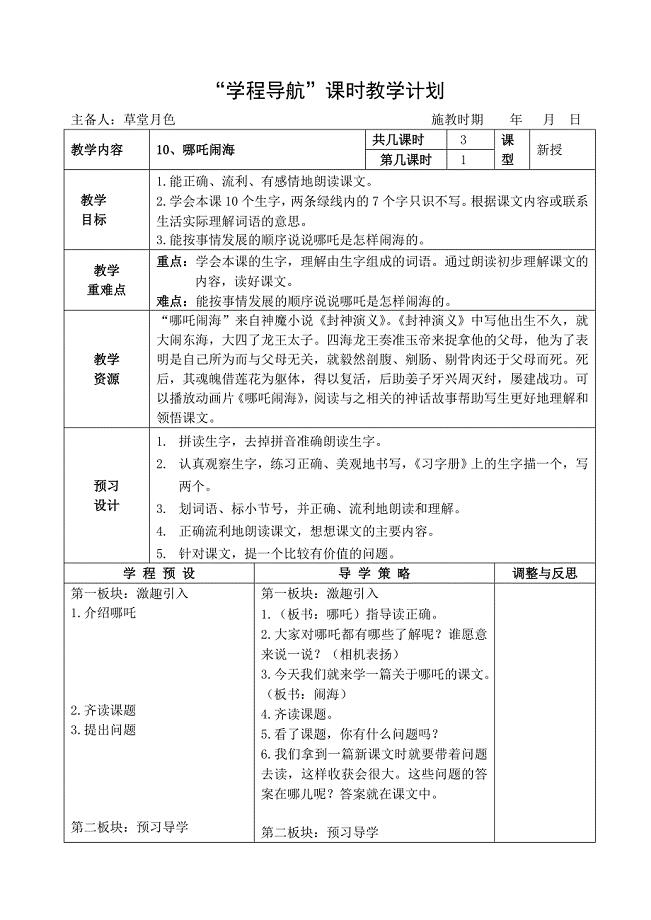

10哪吒闹海第一教时.doc

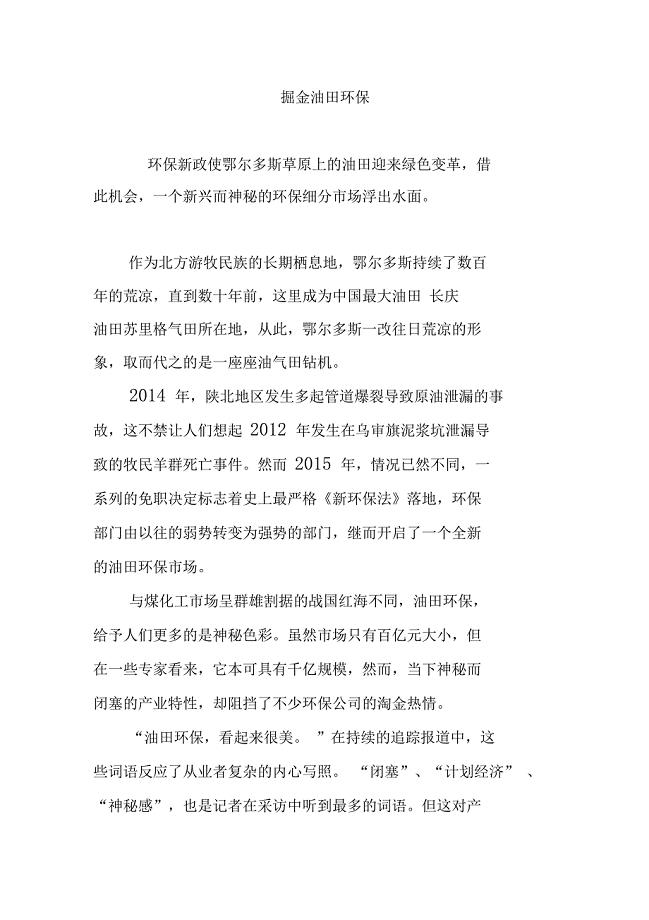

掘金油田环保

【精选】个人建ۥ房管理试行规定精选.doc

应用写作复习试题

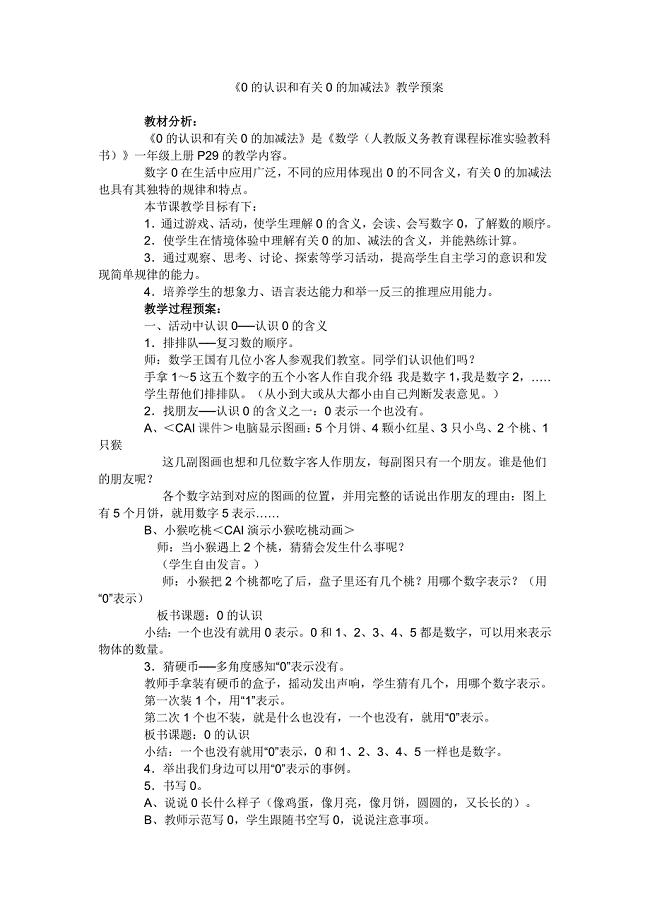

0的认识及有关0的加减法.doc

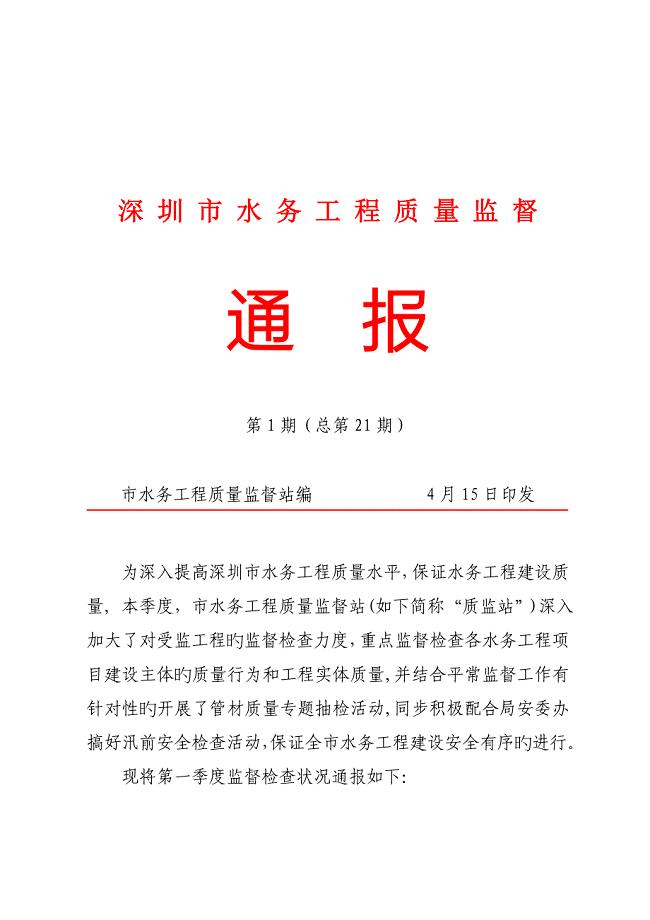

深圳市水务工程质量监督.doc

路基填筑路段施工方案

路基填筑路段施工方案

2022-12-04 11页

世界历史复习专题精编

2023-12-21 12页

排列组合常见题型及解题策略

2023-05-09 10页

2023年企业类会计继续教育考试

2023-04-07 4页

企业文化的四种类型

2023-04-05 2页

企业的财务活动是指货币资金收支活动

2024-01-30 2页

南开大学21春《国际贸易实务》离线作业一辅导答案50

2023-09-28 11页

2018一建机电真题及答案

2023-09-18 9页

福建师范大学21春《艺术设计概论》在线作业二满分答案23

2022-09-01 17页

贸大翻硕——2015年对外经济贸易大学翻译硕士考研真题汇编

2023-03-08 10页